A family dental plan is a shared insurance or membership program that covers multiple family members under one policy to reduce and manage dental care costs across all ages. Most plans follow the industry standard 100-80-50 coverage model, meaning preventive care is covered at 100%, basic services at 80%, and major procedures at 50%. Understanding this structure is the fastest way to avoid surprises when a bill arrives. Cwddentalgroup works with families in Tallahassee to make sense of these options and connect them with care that fits their coverage.

What does a family dental plan explained actually cover?

Family dental plans divide services into three categories: preventive, basic, and major. Each category carries a different coverage percentage and cost-sharing arrangement.

Preventive care includes cleanings, exams, and X-rays. PPO plans cover preventive care immediately with no waiting period, and most plans pay 100% of these costs when you use an in-network provider. This is the category where families get the clearest return on their premium dollars.

Basic services cover fillings, simple extractions, and periodontal treatments. Plans typically reimburse 70–80% of the cost after your deductible. That means a $300 filling could leave you paying $60 to $90 out of pocket.

Major services include crowns, bridges, dentures, and root canals. Coverage drops to around 50%, and annual maximum limits between $1,000 and $2,500 per person apply. Once you hit that cap, you pay 100% of remaining costs for the rest of the benefit year.

Here is what families typically pay beyond their premiums:

- Premiums: $25 to $60 per month for an individual plan, more for family tiers

- Deductibles: Usually $50 to $100 per person before coverage kicks in for basic and major work

- Coinsurance: Your share of the bill after the deductible, typically 20–50% depending on service type

- Annual maximum: The ceiling on what the plan pays per person per year, often $1,000 to $2,500

Pro Tip: If a family member needs a crown and a root canal, ask your dentist whether you can split the procedures across two calendar years. This effectively doubles your usable annual maximum and can save hundreds of dollars.

What types of family dental plans are available?

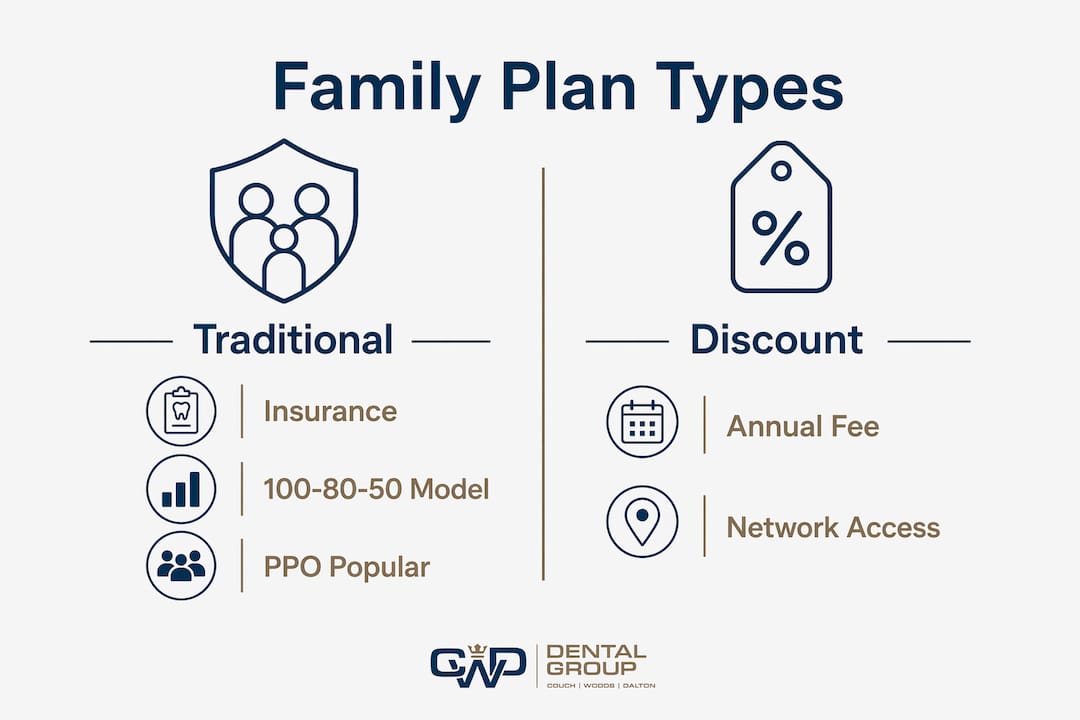

Three main plan types exist for families: traditional dental insurance, dental discount plans, and in-office membership plans. Each serves a different financial situation.

Traditional dental insurance follows the 100-80-50 model described above. PPO plans represent about 80% of individual and family dental plans purchased in the U.S. They offer the widest network access but come with waiting periods of 6 to 12 months for major services.

Dental discount plans are not insurance. They charge an annual membership fee and give you access to a network of dentists who agree to charge reduced rates. Discount plans charge $80 to $200 per year for individuals and $150 to $400 for families, with discounts ranging from 15% to 60%. There are no deductibles, no claims, and no waiting periods. You pay the discounted rate directly at the time of service.

Dental discount plans often save more for families who need immediate major work, since traditional insurance would make them wait 6 to 12 months before covering those procedures.

In-office membership plans are offered directly by dental practices. These plans typically cost $200 to $400 per year, cover preventive care, and offer discounts on all other services with no waiting periods. They work best for families with stable dental needs who want predictable costs and a simpler experience.

| Feature | Traditional insurance | Discount plan | In-office membership |

|---|---|---|---|

| Annual cost (family) | Varies by premium | $150 to $400 | $200 to $400 |

| Waiting periods | Yes, 6–12 months for major | None | None |

| Claims process | Yes, through insurer | No | No |

| Preventive coverage | 100% in-network | Discounted rate | Included |

| Best for | Routine and predictable care | Immediate major needs | Stable, ongoing care |

The right choice depends on your family's current oral health, how soon you need treatment, and how much administrative complexity you want to manage.

Who is covered under a family dental plan?

A family dental plan typically covers the primary subscriber, their spouse or domestic partner, and dependent children. Coverage for dependents usually ends at age 19, though many plans extend to age 26 for full-time students. Some plans also extend coverage for dependents with qualifying disabilities regardless of age.

Common eligibility points families often miss:

- Spouse or partner: Most plans include them automatically, but some employer plans require proof of marriage or domestic partnership.

- Children: Biological, adopted, and stepchildren are typically covered. Foster children may require additional documentation.

- Student extensions: A dependent aged 19 to 26 may stay on the plan if enrolled full-time in an accredited school. You usually need to submit proof of enrollment annually.

- Orthodontic coverage: Orthodontic benefits often carry age restrictions and lifetime dollar caps. Many plans only cover orthodontics for children under 18 and exclude adults entirely.

Pro Tip: Before counting on braces coverage for your child, check whether the orthodontic benefit is a lifetime cap or an annual limit, and whether it applies per person or per family. Many families miss this detail and face unexpected out-of-pocket costs mid-treatment.

A common misconception is that the family annual maximum is shared. In most PPO plans, each covered member has their own annual maximum. That means a family of four could collectively access $4,000 to $10,000 in annual benefits if each member has a $1,000 to $2,500 cap.

How can families choose the right dental plan?

Choosing a dental plan requires matching your family's actual oral health needs to the plan's cost structure. A family with young children who need routine cleanings has very different needs from a family where a parent requires a crown or implant.

Follow this process to narrow your options:

- List your family's likely treatments for the next 12 months. Include routine cleanings, any known restorative work, and orthodontic needs. This gives you a realistic cost baseline.

- Calculate total annual cost, not just the monthly premium. Add premiums, deductibles, and your expected coinsurance share. A lower premium plan with a high deductible can cost more overall if your family uses dental care regularly.

- Check the provider network. Dental insurance works best when your preferred dentist is in-network. Out-of-network visits can cost significantly more, and some plans offer no out-of-network benefits at all.

- Review waiting periods against your timeline. If a family member needs a crown in the next three months, a plan with a 12-month waiting period for major services offers no help for that procedure.

- Compare annual maximums to your projected costs. If your family's projected dental costs exceed $2,500 per person, a discount plan or in-office membership may deliver better real-world value than traditional insurance.

Pro Tip: Ask your dentist's office for a pre-treatment estimate before committing to a plan. Most dental offices will run your proposed treatment through a plan's fee schedule so you can see your actual out-of-pocket cost before you sign up.

Geographic convenience matters more than families realize. A great plan with no in-network dentists near your home or your children's school creates a practical barrier to using it. Cwddentalgroup serves families in Tallahassee with a full range of services, making it easier to stay in-network and use your benefits consistently. You can also review the dental budget planning guide for a detailed breakdown of how to align coverage with your household spending.

What pitfalls should families avoid with dental plans?

The biggest mistake families make is assuming their plan covers more than it does. Annual maximums have remained largely stagnant since the 1970s. Splitting major treatments across two calendar years effectively doubles your usable coverage, and this is one of the most underused strategies in family dental planning.

Watch for these common pitfalls:

- Ignoring waiting periods: Signing up for a plan and immediately scheduling a crown will result in a denied claim if the plan has a 12-month major services waiting period.

- Skipping preventive visits: Preventive care is almost always covered at 100%. Skipping cleanings means leaving a fully covered benefit unused while increasing the risk of needing more expensive treatment later.

- Misreading orthodontic limits: Orthodontic coverage surprises are among the most common family dental plan complaints. Always confirm whether the cap is lifetime or annual, and whether it covers adults.

- Overlooking FSA and HSA accounts: A Flexible Spending Account or Health Savings Account lets you pay dental costs with pre-tax dollars. Pairing an FSA or HSA with your dental plan reduces your effective out-of-pocket cost on every procedure.

Pro Tip: Request a pre-authorization or pre-treatment estimate from your insurer before any procedure over $300. This document confirms what the plan will pay and what you owe, so there are no billing surprises after treatment.

Staying on top of preventive dental visits is the single most cost-effective habit a family can build. Two cleanings per year, covered at 100%, catch problems early and keep major treatment costs low.

Key Takeaways

A family dental plan delivers the most value when families understand its structure, use preventive benefits fully, and time major procedures strategically around annual maximums.

| Point | Details |

|---|---|

| Standard coverage model | Most plans follow 100-80-50: preventive fully covered, basic at 70–80%, major at 50%. |

| Annual maximum matters | Per-person caps of $1,000 to $2,500 reset yearly; split large procedures across two years to maximize benefits. |

| Three plan types exist | Traditional insurance, discount plans, and in-office memberships each suit different family needs and timelines. |

| Orthodontic limits are tricky | Always confirm whether orthodontic caps are lifetime or annual and whether they cover adults or children only. |

| Network access drives real savings | In-network negotiated rates often save more than coverage percentages alone; always verify your dentist is in-network. |

What I've learned from watching families navigate dental coverage

Most families pick a dental plan the same way they pick a phone plan: they look at the monthly price and stop there. That approach almost always costs more in the long run.

The detail that trips up families most often is the annual maximum. A $1,500 cap sounds reasonable until a family member needs a crown and a root canal in the same year. Suddenly the plan that looked affordable on paper leaves you with a $1,200 bill. The families who avoid this are the ones who read the fine print on waiting periods, ask their dentist for pre-treatment estimates, and schedule large procedures with the benefit year in mind.

The other thing I see consistently is families undervaluing preventive care. Two cleanings a year, covered at 100%, are not just a freebie. They are the mechanism that keeps your family out of the major services category. A cavity caught at a cleaning costs a fraction of what a root canal costs after that cavity is ignored for two years.

My honest advice: treat your dental plan as a preventive care tool first and a financial safety net second. If you need significant restorative work soon, a discount plan or in-office membership will serve you better than traditional insurance with a waiting period. Match the plan to your actual situation, not to the lowest monthly number on the comparison page.

— Kayle

Cwddentalgroup is here when your family needs dental care

Choosing the right coverage is only half the equation. The other half is having a dental team that works with your plan and your schedule.

Cwddentalgroup serves families across Tallahassee with a full range of dental services, from routine preventive visits to advanced restorative work. The practice offers same-day emergency appointments, so a cracked tooth or sudden pain does not mean days of waiting. Whether your family has traditional insurance, a discount plan, or no coverage at all, the team at Cwddentalgroup provides transparent pricing and clear treatment estimates before any procedure begins. For urgent situations, Cwddentalgroup's emergency dental care is available when you need it most.

FAQ

What is a family dental plan?

A family dental plan is a single policy that covers multiple family members for dental care, typically including the subscriber, spouse, and dependent children. Most plans follow a 100-80-50 coverage model for preventive, basic, and major services.

How does the annual maximum work in a family dental plan?

The annual maximum is the total amount the plan pays per covered person per year, usually between $1,000 and $2,500. Once a family member hits that cap, they pay 100% of remaining dental costs until the benefit year resets.

What is the difference between dental insurance and a dental discount plan?

Dental insurance reimburses a percentage of covered costs after deductibles and waiting periods. A dental discount plan charges a flat annual fee and gives you access to reduced rates at participating dentists with no claims, no deductibles, and no waiting periods.

At what age do dependents lose coverage on a family dental plan?

Most plans end dependent coverage at age 19, but many extend to age 26 for full-time students. Some plans also continue coverage for dependents with qualifying disabilities beyond standard age limits.

Does a family dental plan cover braces?

Orthodontic coverage varies widely. Many plans cover braces only for children under 18 and apply a lifetime dollar cap rather than an annual one. Adults are frequently excluded. Always confirm the specific orthodontic terms before relying on this benefit.