Dental care family budget planning is the process of forecasting, allocating, and managing funds to cover routine and unexpected dental expenses for every member of your household. Most families underestimate what they will actually spend. National dental spending is projected to exceed $190 billion by 2026, and out-of-pocket costs represent about 38.9% of all dental payouts in the U.S. That means even families with insurance carry a significant share of the bill. Tools like dental insurance from providers such as Humana, discount programs through Cigna, and tax-advantaged accounts like HSAs and FSAs are the core building blocks of any solid family oral health budget.

What does dental care family budget planning actually cost?

The starting point for any family dental budget is knowing what procedures cost before you need them. Average yearly dental spending per American who needs beyond basic care runs around $2,321. Multiply that across a household of four and you are looking at a potential annual exposure of over $9,000 before insurance adjustments.

Costs break down into three tiers. Preventive care, which includes twice-yearly cleanings, exams, and X-rays, runs roughly $200 to $300 per person per year. Basic restorative work such as fillings and simple extractions sits in the $150 to $400 range per procedure. Major procedures like crowns, root canals, and bridges can reach $1,000 to $3,500 per tooth.

Orthodontics is the wildcard that catches most families off guard. Traditional braces for one child typically cost $3,000 to $7,000, and clear aligner systems like Invisalign can run even higher. If you have two children who both need orthodontic work within a few years of each other, that single line item can dwarf every other dental expense combined.

Location matters too. Dental fees in urban markets like New York City or San Francisco run 20% to 40% higher than national averages. Your family's dental history also shapes the forecast. A household with no history of cavities or gum disease will spend far less on restorative care than one managing chronic oral health issues.

| Procedure | Estimated cost per person |

|---|---|

| Preventive exam and cleaning | $200 to $300/year |

| Dental filling (composite) | $150 to $300 per tooth |

| Crown | $1,000 to $1,800 per tooth |

| Root canal (molar) | $1,000 to $1,500 |

| Braces (traditional) | $3,000 to $7,000 per child |

| Teeth whitening (in-office) | $300 to $800 |

Pro Tip: Build your annual dental cost estimate by listing every family member, their last dental visit notes, and any upcoming treatment recommendations. Add those figures before you pick an insurance plan, not after.

Preventive care costing $200 to $300 per year can prevent over $1,000 in restorative costs later. That ratio makes preventive spending the single highest-return line item in any family dental budget.

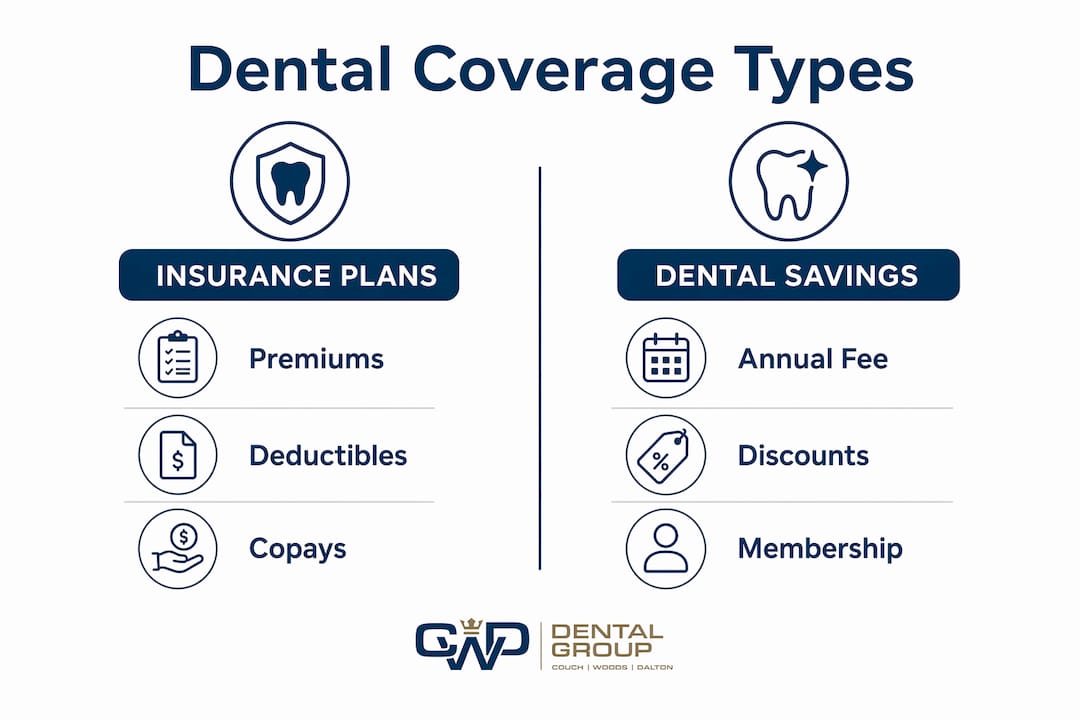

How do dental insurance options affect what your family pays?

Dental insurance is not one product. It is a collection of cost-sharing mechanisms, and understanding each one changes how you budget. Monthly premiums range from $20 to $50 for individuals and $50 to $150 for families, but premiums are only the beginning.

Every plan also carries a deductible, typically $50 to $150 per person, that you pay before coverage kicks in. After the deductible, coinsurance splits remaining costs between you and the insurer. Dental insurance usually covers 100% of preventive care but may only cover up to 80% of basic restorative procedures. Major work like crowns often falls under a 50/50 split. Annual maximums, usually $1,000 to $2,000 per person, cap what the insurer pays in a given year. Once you hit that ceiling, every dollar is yours.

Families tend to underestimate out-of-pocket expenses beyond premiums, including copays and deductibles, which significantly affect total dental spending. A family of four on a plan with a $1,500 annual maximum per person has a combined coverage ceiling of $6,000. If one parent needs a crown and a root canal in the same year, that single member can exhaust their maximum before summer.

| Plan type | How it works | Best for |

|---|---|---|

| PPO | Use any dentist; lower cost in-network | Families wanting flexibility |

| HMO | Must use network dentist; lower premiums | Families with stable providers |

| Indemnity | Pay upfront, get reimbursed | Families in rural areas |

| Discount plan | Annual fee, discounted rates, no insurance | Uninsured or underinsured families |

Orthodontic coverage is a separate rider on most plans and often carries a lifetime maximum of $1,000 to $1,500 per child. That sounds helpful until you see a $5,000 braces quote. Read the fine print on waiting periods too. Many plans impose a 6 to 12 month wait before covering major procedures, which means a family that enrolls in January may not have crown coverage until the following year.

Pro Tip: When comparing plans, calculate your total annual cost by adding 12 months of premiums plus the deductible plus your estimated coinsurance on any planned procedures. The plan with the lowest premium is rarely the cheapest plan overall.

For a deeper look at how dental insurance covers cleanings and what that means for your annual budget, the breakdown is worth reviewing before open enrollment.

What are dental savings plans and when do they make sense?

Discount dental programs are annual fee-based memberships that give you immediate access to reduced rates at participating dentists. Discount dental programs are not insurance and require out-of-pocket payment for services, but they carry no waiting periods, no annual maximums, and no claim forms.

Here is how the math typically works. You pay an annual membership fee, usually $80 to $200 for a family, and in return you receive discounts of 10% to 60% on procedures at network dentists. A cleaning that costs $200 at full price might cost $120 under a discount plan. A crown priced at $1,500 could drop to $900.

Discount plans make the most sense in four specific situations:

- Your family has no employer-sponsored dental coverage and individual insurance premiums are high relative to your expected usage.

- You need a procedure immediately and cannot wait out an insurance plan's waiting period.

- Dental savings plans cover procedures not included in your insurance, such as cosmetic dentistry, offering additional savings on top of your existing plan.

- You are a self-employed family where HSA and HDHP combinations already cover major medical but dental remains uninsured.

The key budget consideration is that discount plans require budgeting for the annual fee plus the actual service costs. Unlike insurance where you pay a premium and the insurer absorbs a share of the bill, a discount plan reduces your bill but you still pay it in full at the discounted rate. Families should model both scenarios with their expected procedure list before choosing.

How to build a practical family dental budget that covers everyone

A family dental budget that actually works requires five concrete steps, not a rough estimate jotted on a napkin.

-

List every family member and their current dental status. Pull the most recent treatment notes or call your dentist's office. Note any recommended but deferred work, upcoming orthodontic consultations, and the age of any existing crowns or fillings that may need replacement.

-

Estimate annual preventive costs first. Two cleanings and exams per person per year is the baseline. For infant dental care and young children, factor in fluoride treatments and sealants, which add $30 to $60 per visit.

-

Add a restorative and emergency reserve. Budget at least $500 to $1,000 per adult per year for unexpected restorative work. Dental emergencies, a cracked tooth, a lost filling, or an abscess, do not schedule themselves. Cwddentalgroup in Tallahassee offers same-day emergency appointments, which protects families from the compounding cost of delayed treatment.

-

Layer in your coverage tool. Subtract what your insurance or discount plan covers from your gross estimate. Add back your annual premium or membership fee. The result is your true net dental cost for the year.

-

Use tax-advantaged accounts to reduce the after-tax cost. IRS Publication 502 confirms that qualifying dental expenses can be itemized for tax deductions, and HSA or FSA contributions reduce your taxable income dollar for dollar. A family in the 22% tax bracket who runs $3,000 in dental expenses through an FSA saves $660 in federal taxes alone.

Pro Tip: Set a calendar reminder each October to review your dental budget for the coming year. Open enrollment for most employer plans closes in November, and your dentist can give you a treatment plan estimate before you commit to a plan.

Community dental clinics offer low-cost services for both children and adults and serve as a practical safety net when insurance or savings plans fall short. Many dental schools also provide supervised care at 40% to 60% below market rates. These resources belong in every family's backup plan. For families in the Tallahassee area, reviewing local dental office options can surface providers who offer sliding-scale fees or payment plans.

Understanding how dental pricing works across different provider types also helps families negotiate or compare quotes before committing to a treatment plan.

Key takeaways

Effective family dental budget planning combines accurate cost forecasting, the right coverage tool, and a tax-smart payment strategy to minimize what your household pays out of pocket each year.

| Point | Details |

|---|---|

| Preventive care pays off | Spending $200 to $300 per person annually prevents over $1,000 in restorative costs. |

| Insurance has a ceiling | Annual maximums of $1,000 to $2,000 per person mean major work often exceeds coverage. |

| Discount plans fill gaps | Cigna and similar programs cover procedures insurance excludes, with no waiting periods. |

| Tax accounts lower real cost | HSA and FSA contributions reduce taxable income, cutting the true cost of dental care. |

| Emergency reserves matter | Budget $500 to $1,000 per adult annually for unplanned restorative or urgent care. |

Why I think most families budget for dental care too late

I have spent years watching families make the same mistake. They pick a dental insurance plan during open enrollment based on the monthly premium alone, then spend the rest of the year surprised by bills. The premium is the least important number in the equation. The deductible, the coinsurance split, and the annual maximum are what determine your actual exposure.

The other pattern I see constantly is families treating orthodontics as a future problem. Braces for two children, spaced three years apart, can represent $10,000 to $14,000 in total costs. That is a predictable expense with a predictable timeline. Families who start a dedicated savings account when their children are seven or eight arrive at the orthodontist's office with options. Families who wait arrive with stress.

Discount plans are genuinely underused. Most families have never heard of them, and the ones who have assume they are a lesser substitute for real insurance. They are not. For a family that needs cosmetic work, or one that has maxed out their insurance annual maximum mid-year, a Cigna discount membership can save hundreds of dollars on the remaining procedures. The two tools work better together than either does alone.

The families I have seen manage dental costs most effectively share one habit. They treat their dental budget as a living document, not a one-time calculation. They revisit it every fall, update it based on treatment recommendations, and adjust their coverage choices accordingly. That single habit, more than any specific plan or provider, is what keeps dental costs from becoming a financial crisis.

— Kayle

How Cwddentalgroup helps Tallahassee families manage dental costs

Cwddentalgroup is built around the reality that dental emergencies and routine care both need to fit into a real family budget. They accept most major insurance plans and offer flexible payment options so that cost does not become a barrier to necessary treatment.

For urgent situations, Cwddentalgroup provides same-day emergency dental care in Tallahassee, which prevents the compounding costs that come from delaying treatment. A cracked tooth addressed the same day costs far less than an abscess treated a week later. Their team can also walk families through treatment cost estimates and help identify which services fall under their current insurance coverage, making the budgeting process concrete rather than guesswork. Contact Cwddentalgroup to discuss your family's dental needs and build a care plan that fits your budget.

FAQ

How much should a family of four budget for dental care annually?

A family of four should budget between $2,000 and $5,000 per year for dental care, depending on insurance coverage, the ages of children, and any planned restorative or orthodontic work. Families with children approaching orthodontic age should add a separate savings line for braces costs.

Is dental insurance worth it for families?

Dental insurance is worth it for most families because it covers 100% of preventive care and reduces costs on restorative procedures, but the annual maximum of $1,000 to $2,000 per person means it does not cover major work in full. Pairing insurance with an HSA or FSA maximizes the financial benefit.

What is the difference between a dental savings plan and dental insurance?

A dental savings plan is an annual membership that provides discounted rates at participating dentists, while dental insurance is a cost-sharing contract with premiums, deductibles, and annual maximums. Savings plans have no waiting periods and no claim forms, but you pay the full discounted rate out of pocket at each visit.

Can dental expenses be deducted on taxes?

Yes. According to IRS Publication 502, qualifying dental expenses can be itemized as medical deductions on Schedule A of Form 1040, which reduces taxable income for families who exceed the standard deduction threshold.

How do I budget for unexpected dental emergencies?

Set aside $500 to $1,000 per adult annually in an HSA or dedicated savings account to cover unplanned restorative work or emergency visits. Families near providers like Cwddentalgroup who offer same-day appointments can also avoid the higher costs associated with delayed emergency treatment.